Welcome to the 38 new subscribers who have joined us since yesterday! If you aren’t subscribed, join 497 smart, curious folks by subscribing here:

Our last post talked about how option value = intrinsic value + extrinsic value.

Please here out the previous post on pricing an option and determinants of options price (1) if you haven't! It’s important to learn what grinds the gears of this tool to use it efficiently.

Today, we are going to focus on extrinsic value. Also known as time value.

Extrinsic value is determined by 2 factors: (1) Time left until the option expires, and (2) Implied Volatility (IV)

(1) Time left until the option expires

Simply put, if I buy a call option that expires in July 2021, the 6 months between now and Jul 2021 are gonna be worth something. Because I’m purchasing insurance for 6 months.

A contract loses value as it approaches its expiration date because there’s less time for the underlying stock to move favorably.

(2) Implied Volatility

IV measures how much the stock price moves. The more violent the stock price, the higher the IV, and therefore the more expensive the option (higher extrinsic value).

This means that for a company like Fastly, buying an option will expensive due to huge movements in stock prices.

Compare this to Berkshire, buying an option will be cheaper due to the relatively stable stock prices.

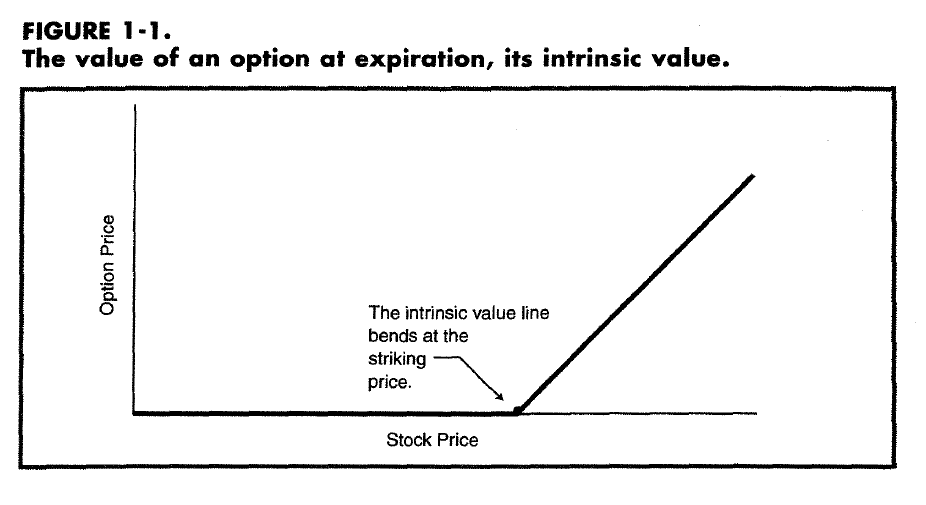

Viewing intrinsic value on a chart

An option with only intrinsic value would look like this:

The option price will start to turn upwards after the underlying stock price exceeds the strike price.

Viewing extrinsic value on a chart

An option with both intrinsic value and extrinsic value would look like this:

The shaded area is the extrinsic value of the option.

When to buy (or sell) insurance?

Options are a good way to protect your portfolio. But similar to insurance, if you only buy after you need it, you are going to pay a steep price.

A huge portion of the options pricing is going to be based on implied volatility. Meaning once the price of your stocks starts swinging violently (in both directions), the options prices are going to shoot up.

When paired with sound fundamental analysis, there resides a solid opportunities for investors.

For example, in Mar 2020 when the market was crashing, I would be comfortable selling long-dated puts on Berkshire and collect the premiums. They have a fortress of a balance sheet (> $100 billion in cash) and was significantly undervalued.

In my future posts, I will talk about how you could sell puts to pay for your buy calls. This will help you capture your gains in case the market rebounded before your sell puts could be exercised.

Thanks for reading!

If you have found this useful, please share it with your friends! It would encourage me to share more about what I learned on options :)